Agentic AI in Embedded Finance: How Non-Financial Apps Are Building Lending, Cards, and Wallets

Quick Summary Embedded finance is transforming how non-financial apps deliver financial services. Powered by agentic AI, modern SaaS products, marketplaces, and mobile apps are building lending, digital cards, and wallets directly into their platforms without becoming banks. This guide explains what embedded finance is, how agentic AI supercharges it, the tech stack you need, real […]

Apr 17, 202612 min read

Apr 17, 202612 min read

Quick Summary

Embedded finance is transforming how non-financial apps deliver financial services. Powered by agentic AI, modern SaaS products, marketplaces, and mobile apps are building lending, digital cards, and wallets directly into their platforms without becoming banks. This guide explains what embedded finance is, how agentic AI supercharges it, the tech stack you need, real use cases, regulatory considerations, cost estimates, and a 60-day action plan to launch your own embedded finance features.

The global embedded finance market is projected to reach $7 trillion by 2030, according to Dealroom research. That growth is not coming from traditional banks; it is coming from Shopify, Uber, Amazon, and thousands of smaller SaaS products that have quietly added loans, cards, and payment accounts to their platforms.

The reason this is possible today and was not five years ago: Banking-as-a-Service (BaaS) providers handle the regulatory and banking infrastructure, while agentic AI handles the intelligence credit underwriting, fraud detection, personalization, and autonomous compliance monitoring. Together, they let any app become a financial product overnight.

At Metizsoft, with 13+ years of experience serving fintech clients including PayGlocal, we have helped multiple non-financial platforms embed lending, digital wallets, and card products using agentic AI architectures. This guide shares the complete playbook we use.

What Is the Role of Agentic AI in Embedded Finance?

Embedded finance means integrating financial services, such as payments, lending, insurance, wallets, and cards, directly into a non-financial product. When Shopify offers merchant loans, when Uber drivers get instant payouts to a branded debit card, and when an HR platform lets employees access earned wages, that is embedded finance.

Agentic AI is what makes embedded finance scalable. Without intelligent automation, every loan application, fraud check, or compliance review would need manual human review, which breaks the economics. With agentic AI, these decisions happen autonomously in seconds based on proprietary data the host platform already has about its users’ purchase history, behavior patterns, and transaction flows.

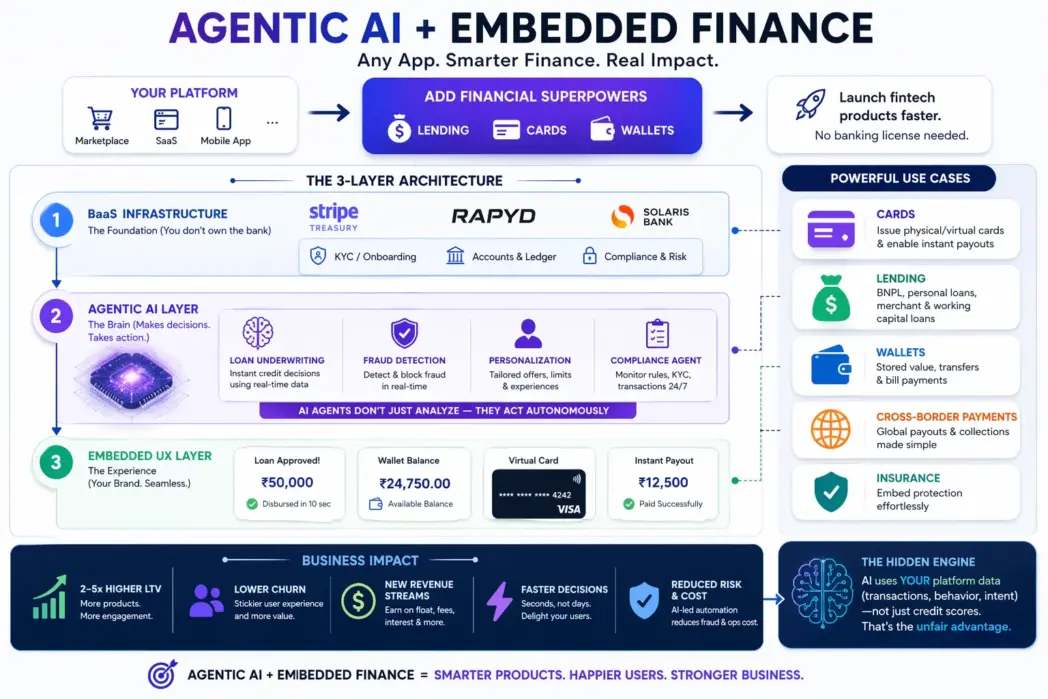

The three layers of modern embedded finance

- BaaS infrastructure: companies like Stripe Treasury, Unit, Rapyd, and Solaris provide the regulated banking backend (KYC, account issuance, card rails, compliance). You do not need a banking license.

- Agentic AI decision engine: autonomously underwrites loans, scores fraud risk, personalizes offers, monitors transactions, and handles customer support. This is where custom AI development adds the most value.

- User-facing integration: the embedded experience inside your app, apply-for-loan flow, card issuance UI, wallet management, instant transfer buttons. This lives inside your existing product.

Why Are Non-Financial Apps Embedding Finance Now?

Three forces have converged in the last 24 months. First, BaaS providers have matured enough to handle enterprise-grade volume with compliance already built in. Second, agentic AI systems have become accurate enough for real-time credit and fraud decisions without human intervention. Third, customer expectations have shifted; users now expect to complete financial tasks without leaving the app they are already in.

The business case is strong. Platforms that embed finance see 2-5x higher customer lifetime value, significantly lower churn (because the user now depends on the platform for money movement), and entirely new revenue streams through interchange, interest, and platform fees.

The PayGlocal example

Metizsoft partnered with PayGlocal, a cross-border payment platform, to build intelligent payment flows that handle currency conversion, compliance routing, and fraud detection in real-time. This is the kind of agentic AI-first fintech infrastructure every modern platform needs.

What Are the Top Embedded Finance Use Cases?

1. Agentic AI lending and BNPL

B2B SaaS platforms offer working-capital loans to their users based on revenue patterns. B2C apps offer Buy-Now-Pay-Later at checkout. Agentic AI underwrites these loans autonomously in under 5 seconds using platform data not traditional credit bureau scores. Examples: Shopify Capital, Square Capital, Affirm.

2. Branded debit cards and instant payouts

Gig economy platforms issue branded cards so drivers or freelancers can access earnings instantly. Agentic AI detects unusual spend patterns, flags potential fraud autonomously, and personalizes rewards. Examples: Uber Pro Card, DoorDash DasherDirect, Lyft Direct.

3. Digital wallets and stored value

Platforms let users maintain a wallet balance for faster transactions, rewards, and peer-to-peer transfers. Agentic AI systems handle fraud scoring on every transaction and predict which users are ready to adopt wallet features. Examples: Starbucks app, WeChat Pay, PayPal wallet.

4. Embedded insurance

E-commerce checkouts offer shipping insurance, ride-hailing apps offer trip insurance, and property platforms offer renter coverage. Agentic AI prices risk dynamically based on context item value, route, neighborhood, and user history. Examples: Cover Genius, Sure, Qover.

5. Cross-border payments with agentic AI routing

Marketplaces and SaaS platforms send money internationally through agentic AI that picks the optimal corridor based on fees, speed, and compliance. The system continuously re-optimizes without human intervention. Examples: Wise for platforms, PayGlocal, Airwallex.

What Tech Stack Do You Need for Agentic AI in Embedded Finance?

The modern embedded-finance-with-agentic-AI stack has three distinct layers. Choose carefully, you will live with this architecture for years.

Layer 1: BaaS provider (the regulated backend)

- Stripe Treasury / Issuing: best for platforms already on Stripe. Strong API, good documentation, US-focused.

- Unit, Synapse, Rapyd: more flexible for card programs and wallets. Global coverage varies.

- Solaris, Railsr, Swan: European leaders for regulated EU fintech products.

- Razorpay, M2P, Zwitch: Indian market leaders for domestic embedded finance.

Layer 2: Agentic AI decision engines

This is where custom AI development adds the most value. Off-the-shelf solutions exist but rarely fit a platform’s unique data and risk profile.

- Agentic underwriting systems: multi-step reasoning agents trained on your platform’s user data. Often outperform traditional FICO-based models by 30-50% on thin-file borrowers.

- Fraud detection agents: graph neural networks for connected-entity detection plus real-time LLM-based transaction analysis for emerging fraud patterns.

- Compliance monitoring agents: autonomous systems that monitor transactions, flag anomalies, and generate regulatory reports without human intervention.

Layer 3: Integration and user experience

- Backend integration layer: your existing APIs wrap BaaS provider APIs. Event-driven architecture (Kafka, AWS EventBridge) handles webhooks reliably.

- User-facing flows: KYC onboarding, loan application, card activation, wallet top-up. These live inside your app, styled to your brand.

- Agentic AI customer support: intelligent assistants trained on your specific product handle 60-70% of support tickets autonomously before escalating to humans.

If you are evaluating off-the-shelf vs custom solutions, read our guide on custom AI vs off-the-shelf AI development for embedded finance. Custom agentic AI almost always pays for itself within 12 months.

What Are the Regulatory Considerations?

Embedded finance is regulated. The BaaS provider handles most compliance, bank license, capital requirements, and deposit insurance, but your platform still has real obligations.

KYC and identity verification

Every user who opens an account, applies for credit, or holds a wallet must be identity-verified. This typically involves government ID scan, liveness detection (selfie video), and database checks against sanctions and PEP lists. Agentic AI-powered KYC providers like Onfido, Jumio, and Veriff handle this in under 60 seconds with 99%+ accuracy.

AML and transaction monitoring

Every transaction must be monitored for money laundering patterns. Agentic AI systems flag suspicious behavior (structuring, layering, rapid fund movement) for human review when escalation is needed. Your platform or BaaS provider files Suspicious Activity Reports with regulators when required.

Data privacy

Financial data is subject to stricter privacy rules than general SaaS data. GDPR in Europe, CCPA in California, and DPDP in India all have specific provisions for financial information. Build privacy-by-design into the architecture from day one.

Explainability of AI decisions

In the US, the Equal Credit Opportunity Act requires lenders to explain adverse decisions. If your agentic AI denies a loan, you must be able to explain why in plain language. Use SHAP values or similar explainability techniques, and always keep a human-in-the-loop option for borderline cases.

What Is the Cost of Agentic AI in Embedded Finance Development?

Realistic cost and timeline estimates based on projects we have scoped for fintech and non-financial platforms:

| Scope | Investment | Timeline |

| Basic wallet + payments (single country) | $80K – $150K | 14-20 weeks |

| Embedded lending with agentic AI underwriting | $180K – $320K | 20-28 weeks |

| Branded card program + agentic fraud detection | $220K – $400K | 24-32 weeks |

| Full embedded finance suite (lending + cards + wallet) | $400K – $800K | 36-52 weeks |

Ongoing costs include BaaS provider fees (typically 0.1-0.5% of transaction volume plus monthly platform fees), agentic AI inference costs ($0.01-$0.05 per decision), and maintenance engineering. Budget roughly 25-30% of the initial build cost annually for ongoing operations.

Hidden cost alert

Most teams underestimate the cost of ongoing compliance, fraud ops, and customer support. Budget a dedicated fraud and compliance team from month six onwards — embedded finance products without active monitoring become loss-making quickly.

How Do You Get Started in the Next 60 Days?

A practical 60-day feasibility and prototype plan for any product team evaluating embedded finance:

- Weeks 1-2: Define the user story. What single financial action does your user need inside your product? Not a list of ten ideas. One focused use case. Interview 10 current users.

- Weeks 3-4: Map the unit economics. For each transaction, what does it cost you (BaaS fees, AI inference, support) and what does it earn (interchange, interest, platform fee)? Build the simple spreadsheet.

- Weeks 5-6: Pick the BaaS provider. Shortlist three providers, get pricing, test their sandbox APIs, and check their country coverage. Do not commit to a contract yet, just validate they can deliver what you need.

- Weeks 7-8: Prototype the agentic AI decision flow. Build a simple underwriting or fraud agent using synthetic or anonymized data. Test accuracy against business rules. This is your AI feasibility check.

- Weeks 9-1: Build a clickable UX prototype in Figma. Test with 10 real users. Confirm the flow makes sense, and the conversion looks plausible.

- Weeks 11-12: Write the investment case and go-or-no-go memo. If the numbers work, move to engineering. If not, you have a well-documented reason to defer, which has value on its own.

Frequently Asked Questions

Do we need a banking license to offer embedded finance?

No. BaaS providers hold the banking license and partner bank relationships. Your platform offers the user experience and owns the agentic AI intelligence layer. The BaaS provider is the regulated entity of record for the financial services.

How long does it take to launch an embedded finance product?

A focused MVP (one product in one country) takes 14-24 weeks. A production-grade multi-country launch typically takes 32-52 weeks. Timeline depends on regulatory approvals, BaaS integration complexity, and how much custom agentic AI development your use case requires.

Can agentic AI really replace traditional credit bureau data for underwriting?

For platforms with proprietary behavioral data, yes, often with better results. Shopify Capital uses merchant transaction history instead of personal credit scores and reports materially lower default rates than traditional SME lending. The key is that the platform already has high-signal data that its users do not share with banks.

What is the biggest risk in embedded finance?

Fraud and regulatory non-compliance. Both compound silently; you can look profitable for months while fraud losses accrue or compliance gaps widen, then face a catastrophic write-off or enforcement action. Invest in agentic AI-powered fraud detection and compliance monitoring from day one, not as a phase-two project.

How does embedded finance differ from being a fintech?

A fintech is a financial services business first. An embedded finance platform is a software business that adds financial services as a feature. Fintechs carry full banking licenses and regulatory capital. Embedded platforms use BaaS partners and focus on a specific user base they already own.

Can an existing SaaS product add embedded finance without rebuilding?

Yes. Most embedded finance features integrate via API at the edges of your existing product. You add new user flows (KYC, application, card activation) and new backend services (BaaS integration, agentic AI decision engine), but your core product does not need to be rebuilt. Expect 8-16 weeks for the initial integration, depending on the scope.

Ready to build embedded finance into your platform?

Metizsoft has 14+ years of experience delivering fintech solutions and has served 1,000+ clients across 25+ countries, including cross-border payment platform PayGlocal. Our dedicated agentic AI and fintech engineering team handles scoping, BaaS integration, AI model development, and compliance architecture. Book a free 30-minute consultation, and we will give you an honest assessment of feasibility, cost, and timeline for your specific use case.

→ Book a free embedded finance consultation with Metizsoft

About Metizsoft

Metizsoft Solutions is a leading AI, ML, and software development company founded in 2012. With 150+ experts, 3,000+ projects delivered, and offices in India, the USA, the UK, and Singapore, we serve clients in 25+ countries. As an ISO-certified company and official Shopify Partner since 2013, we specialize in Agentic AI, AI Development, Machine Learning, NLP, Deep Learning, Generative AI, and AI Agent Development, delivering custom intelligent solutions for fintech, SaaS, logistics, and commerce products worldwide.

Related reading: Agentic AI in Banking │ , AI for Financial Forecasting │ , Agentic AI Lifecycle

Leave a Reply